If you work for yourself, you already know the narrative: “Banks hate self-employed borrowers.” I’ve heard this frustration from countless freelancers, business owners, and 1099 contractors.

But here is the truth—banks don’t hate you; they just need a different way to understand your money.

While a W-2 employee hands over a pay stub and calls it a day, your path involves proving the stability of your income amidst the natural fluctuations of business.

This guide is designed to demystify that process. We are going to move past the myths and focus on the actionable mechanics of getting approved.

In this guide, you will learn:

- How to structure your accounts to satisfy strict underwriter requirements.

- Which documents actually matter (and which ones you can skip).

- Strategic alternatives like Non-QM loans that bypass tax returns entirely.

Whether you are looking to buy your first home or invest in rental property, this roadmap will take you from “application denied” to “clear to close.”

For personalized advice on your specific situation, I also recommend leveraging Bluerate to consult with specialized non-qm loan officers for free.

Step 1: Drawing the Line Between Personal and Business Funds

The most common mistake I see isn’t low income; it’s “messy” income. When an underwriter opens your file, they are acting like a forensic accountant.

If they see you paying for your Netflix subscription out of your LLC’s operating account, or buying business inventory with your personal Visa, they lose confidence in your financial stability.

Here is how to fix it immediately:

- Establish Distinct Accounts: Ensure you have a dedicated business checking account that is completely separate from your personal finances.

- Formalize Your Pay: Don’t just transfer random amounts when you need cash. Set up a scheduled “Owner’s Draw” or salary transfer.

- Use Professional Bookkeeping: Tools like QuickBooks or FreshBooks aren’t just for taxes; they create the clean Profit & Loss statements lenders love.

Why this matters: A clear separation proves your business is a standalone, viable entity. It allows the lender to clearly identify “income” versus “revenue,” making the verification process significantly faster.

Step 2: The Tax Deduction Dilemma: Balancing Write-Offs and Income

As business owners, we are trained to minimize our tax liability. However, a good day for your tax bill is often a bad day for your mortgage application.

Traditional lenders calculate your qualifying income based on your net profit (after expenses), not your gross revenue. If you wrote off everything to show zero profit, you technically have zero income to pay a mortgage.

The Strategy:

- Plan Ahead: If you plan to buy a home in the next two years, consult your CPA about easing up on aggressive (discretionary) write-offs to show a healthier bottom line.

- Identify Add-Backs: Not all deductions hurt you. Non-cash expenses like depreciation or depletion can often be “added back” to your income by the underwriter, boosting your qualifying amount.

Work with your accountant to create a “lender-friendly” view of your finances. You aren’t trying to pay more taxes than necessary; you are trying to optimize your Adjusted Net Income for the bank.

Step 3: Strategic Credit Management for Better Rates

Your credit score is the single biggest factor in determining your interest rate. For self-employed borrowers, a high score also serves as a character witness—it tells the lender, “Even if my income fluctuates, my payment history does not.”

Actionable steps to prep your credit:

- Target the 700+ Club: While FHA loans might accept scores as low as 600–620, getting your score above 700 (and ideally 740) opens up the best conventional and Non-QM rates.

- Manage Utilization: Pay down revolving debt (credit cards) to below 30% of their limits before you apply. This boosts your score and lowers your Debt-to-Income (DTI) ratio.

- Monitor Reports: Check your credit report months in advance. Disputing an error can take 30–60 days, and you don’t want that fight happening during escrow.

Step 4: Building Your Financial Cushion: Down Payments and Reserves

Lenders look for “compensating factors.” Since your income isn’t guaranteed by an employer, having cash on hand reduces the lender’s risk. You need to show that you can weather a business downturn without missing a mortgage payment.

What to prepare:

- The Down Payment: Plan for 10% to 20%. While lower down payment options exist, putting more down can waive certain income requirements or lower your rate.

- Reserves are Key: Lenders often require 3 to 6 months of mortgage payments (PITI) sitting in a liquid account after closing.

- Paper Trails: Ensure all funds are “seasoned” (sitting in your account for 60+ days). If you have a sudden large deposit, be ready to document exactly where it came from (e.g., a specific client invoice or asset sale).

Step 5: Navigating Tax Returns and Income History

If you are applying for a standard Fannie Mae or Freddie Mac loan, your tax returns are the primary evidence of income. The standard requirement is two years of personal and business returns.

Critical considerations:

- The Two-Year Average: Lenders will typically average your net income over the last two years.

- The Trend Matters: If your income increased from Year 1 to Year 2, the average is used. If it decreased, the lender will likely use the lower, most recent year—or worse, decline the loan if the drop is severe.

- Documentation: Have your Schedule C (Sole Proprietorship), Form 1065 (Partnership), or Form 1120S (S-Corp) ready.

If your tax returns show a loss or very low income due to deductions, don’t panic. You are likely a candidate for Non-QM loans (covered in Step 10), which don’t require these tax forms.

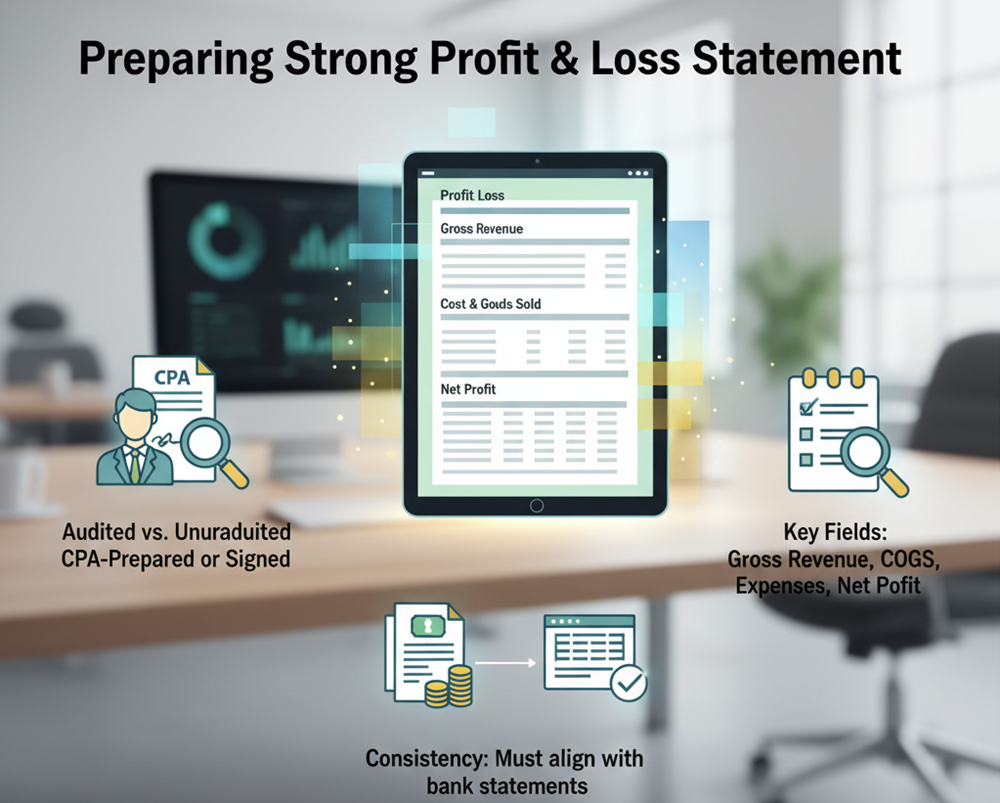

Step 6: Preparing a Strong Profit & Loss Statement

A Profit & Loss (P&L) statement brings your financial story up to date. Since tax returns are historical (looking at last year), the P&L tells the lender how your business is performing this year (Year-to-Date).

How to get it right:

- Audited vs. Unaudited: While you can print a P&L from QuickBooks, lenders overwhelmingly prefer a CPA-prepared or signed P&L. It adds a layer of third-party trust.

- Consistency: The numbers on your P&L must align with the deposits showing in your bank statements. Discrepancies here are a major red flag for underwriters.

- Key Fields: Ensure it clearly breaks down Gross Revenue, Cost of Goods Sold, Expenses, and Net Profit.

Step 7: Using Bank Statements to Validate Cash Flow

For many of us, the bank account shows the real money, not the tax return. Bank Statement Loans are a specific type of financing where lenders use 12 or 24 months of bank deposits to calculate your income.

The Methodology:

- Personal Accounts: Lenders typically count 100% of deposits as income.

- Business Accounts: Lenders will apply an “expense factor” (often assuming 50% is overhead) unless your CPA provides a letter stating your actual expense ratio is lower.

Tip: Review your statements for “non-business” deposits. Transfers from savings, tax refunds, or loans do not count as income. Highlight your client payments to make the underwriter’s job easier.

Step 8: Verifying Your Business Legitimacy

You must prove that your business is not just a hobby. The lender needs to see that you are an active, operating entity with a likelihood of continued income.

Compile your “Business Evidence Pack”:

- Business License: Current city, county, or state registration.

- Online Presence: An active website or professional LinkedIn profile.

- Entity Documents: Articles of Organization (LLC) or Incorporation (Corp).

- Client Contracts: Executed agreements showing future work.

- Invoices: A sampling of paid invoices from the last few months.

Combining these documents creates a narrative of stability and professionalism that reassures the lender.

Step 9: The Essential Supporting Documents Checklist

Beyond the big financial statements, missing small documents can cause agonizing delays. Being proactive here is your superpower.

Get these ready in a digital folder:

- 1099 Forms: For the last two years (if applicable).

- CPA Comfort Letter: A simple letter from your accountant verifying how long you’ve been self-employed and your current ownership percentage.

- Asset Statements: All pages (1-6, even if blank) for checking, savings, and investment accounts.

- ID & Residency History: Driver’s license and a list of addresses for the last 2 years.

- Lease Agreements: If you own other properties, show the rental income.

Step 10: Unlocking Flexibility with Non-QM Loan Programs

If the traditional route feels like a dead end because of your tax write-offs, Non-QM (Non-Qualified Mortgage) loans are the solution.

These are not “subprime” loans; they are smart loan products designed for complex income profiles.

Top Non-QM Options for the Self-Employed:

- Bank Statement Loans: The most popular choice. Uses 12-24 months of personal or business bank deposits to determine income, ignoring tax returns entirely.

- P&L Only Loans: Qualify using only a CPA-prepared Profit & Loss statement.

- 1099 Only Loans: Ideal for gig workers and realtors. Uses the gross income on your 1099 forms to qualify.

- DSCR Loans (Debt Service Coverage Ratio): Specifically for investors. Qualification is based on the property’s rental cash flow covering the mortgage payment, not your personal income.

- Asset-Based / Asset Depletion: Uses your liquid assets (stocks, savings, retirement) divided over a loan term to create a “phantom” monthly income.

- ITIN Loans: For borrowers without a Social Security Number.

- Foreign National Loans: For non-US citizens investing in US property.

Note: These loans often require a higher down payment (e.g., 20%) and may have slightly higher rates, but they make homeownership possible when tax returns say “no.”

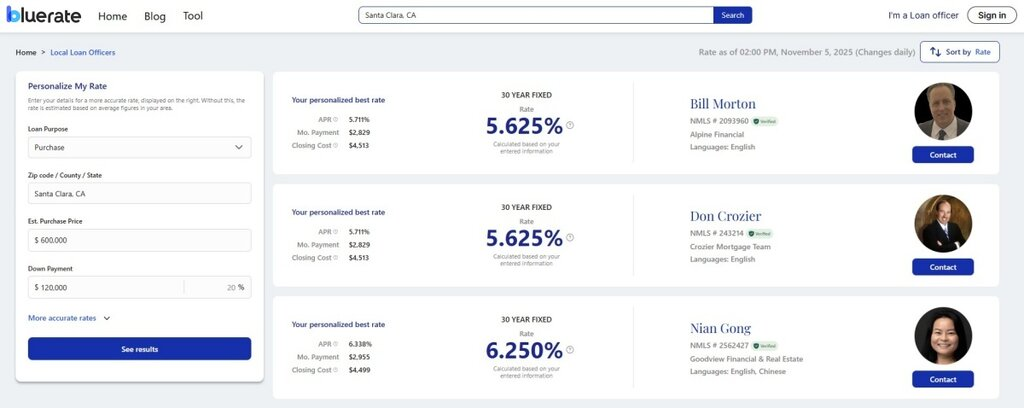

Step 11: Finding the Right Lender and Comparing Offers

Not all lenders know how to handle self-employed borrowers. A big bank might reject you simply because their automated system doesn’t understand your Schedule C. You need a specialist.

Your Shopping Strategy:

- Get Multiple Quotes: Aim for 3-5 Loan Estimates. Compare the APR, not just the interest rate, as APR includes closing costs.

- Ask Hard Questions: Ask the loan officer, “How many self-employed loans have you closed this month?” Experience matters.

To streamline this, I highly recommend using Bluerate. It is an AI Mortgage Marketplace that solves the biggest pain points of shopping for a Non-QM loan:

- Borrower Autonomy: You aren’t randomly assigned. You get matched with local non-qm loan officers and you choose who to contact for free.

- No “Teaser” Rates: The rate you see is the rate you get. Bluerate prioritizes real data over marketing fluff.

- Massive Data Access: They connect with nearly 30 mainstream lenders to update rates in real-time.

- Instant Personalization: Input your credit score, down payment, and income to get a Personalized Rate calculation instantly—no guessing.

- Faster Closing: Their integration with Loan Origination Systems (LOS) lets you track every step of the process, which can help close your loan up to 20% faster than traditional methods.

Final Thoughts: Your Roadmap to Closing

Being self-employed shouldn’t disqualify you from the American Dream. In fact, your business savvy is exactly what makes you a great homeowner. The key is preparation.

By separating your finances, organizing your documentation, and choosing the right loan program, you turn the “risk” of self-employment into a verifiable asset.

Here are your 2 immediate action items:

- Organize Your Paperwork: Download your last 12 months of bank statements and scan your business license today.

- Connect: Use Bluerate to start a conversation with a specialized loan officer who understands Non-QM products.

Don’t let the paperwork scare you. With the right guide and the right tools, you are closer to your new front door than you think.